County staff outline solid waste budget, landfill valuation method and closure fund balances

Get AI-powered insights, summaries, and transcripts

Sign Up Free

Summary

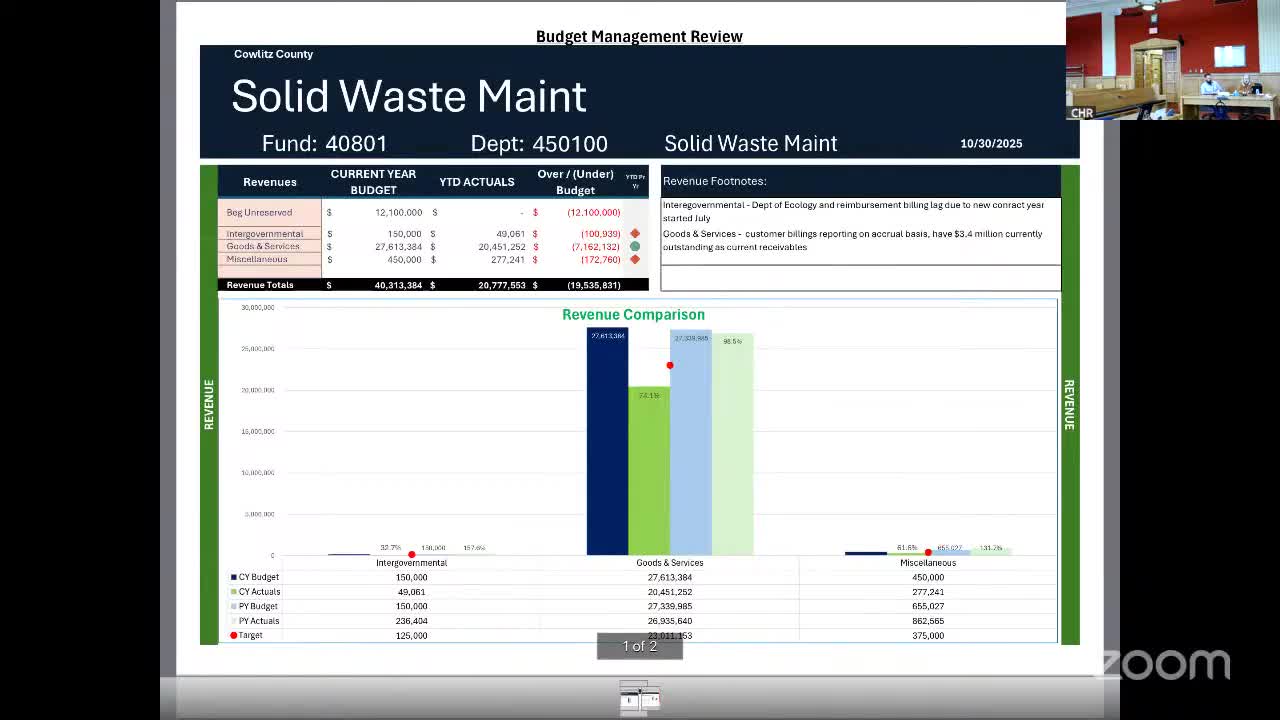

Finance and public works staff told commissioners the solid waste budget is roughly $27M in projected revenue with current receivables about $3.45M, and explained the county's 6% return methodology for valuing landfill rent.

Cathy (Kathy Funk Baxter, Finance Director, Speaker 5) and Sean (Public Works, Speaker 8) briefed commissioners on multiple solid waste accounts including customer billings, a Spillman software pass‑through, and capital budgets for landfill projects. Key figures: accrual accounting shows roughly $3.45M in current receivables for customer billings that staff expect to collect in coming months; the 2026 budget for solid waste revenue is roughly $27M and expenses are close to that level when transfers are included.

On landfill valuation, staff explained the county uses a remaining‑capacity valuation with a 6% return assumption (used historically and recommended by legal counsel and auditors) to calculate annual rent from landfill value; that method currently produces about $7.5M in annual rent rather than an $8M maximum that could be charged. Staff said the 6% assumption has been reviewed during budget cycles (last reviewed while preparing the 2025 budget) and that the figure is meant to be consistent over time. Capital items discussed include a vertical gas well project (~$1.7M) and ongoing design for a future cell (Cell 10). Closure and post‑closure funds hold roughly $19M in balances and earn interest that staff aim to use to reduce annual transfer requirements. Commissioners asked for a city‑by‑city breakdown of transfer subsidies and for further analysis on rent and capacity assumptions.