Presenter says state retirement plans are on track while noting COLA caps, rehiring limits and Social Security changes

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

A staff presenter told a legislative committee the state’s major retirement plans have strengthened, with projected combined surpluses, while describing cost-of-living limits, a cap on rehire hours for retirees and the expected effect of the Social Security Fairness Act.

Noah Pringle, a staff member, told a legislative committee that the state’s major public retirement plans have strengthened and are projected to move into combined surpluses over the budget outlook period, but he highlighted several limits and recent legal and policy changes that affect retirees.

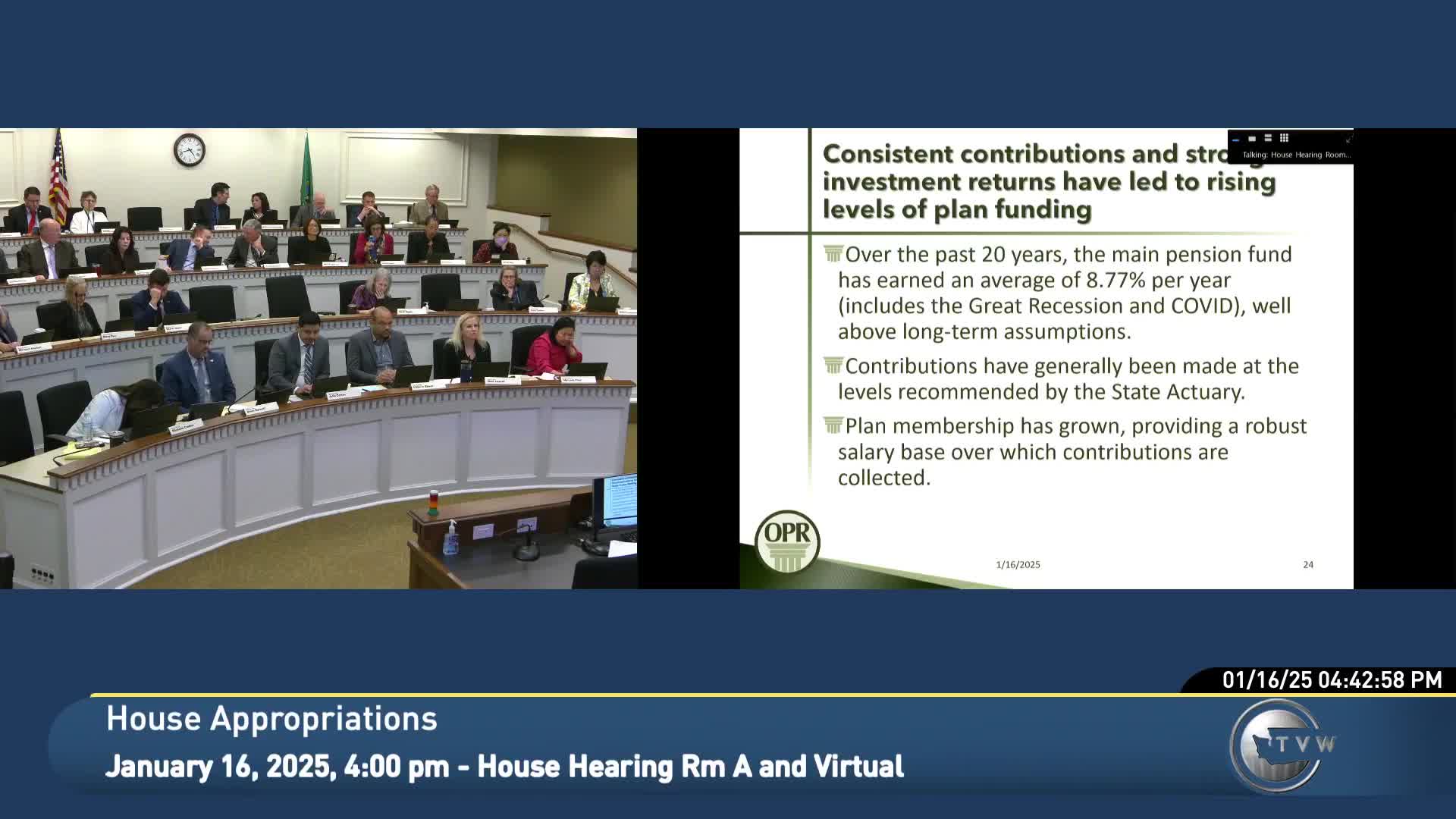

"Around 8.8% per year. And this along with, you know, consistently con contributing to the pension plan, state and employers, at levels at or near that was recommended by the state actuary and plans, the growth in plan membership has led to the plan's overall financial condition continuing to strengthen," Pringle said, describing recent contribution and salary-base growth that increased total contributions to the plans.

Pringle said the Pension Funding Council’s 2021 decision to lower the assumed investment rate of return from 7.5% to 7% increased measured liabilities, while a 2020 legislative directive to deposit $250 million into the Teachers' Retirement System (TRS) Plan 1 fund reduced that plan’s unfunded liability. He told the committee that under current projections the combined plans would move from roughly even to a multi‑billion dollar surplus over the outlook period.

Why it matters: the funding status affects the state budget, K‑12 allocations used for teacher pay, and estimates of future contribution requirements.

Pringle summarized several program details committee members asked about. He said Public Employees’ Retirement System (PERS) and TRS Plan 1 had projected unfunded liabilities of about $500 million each on an actuarial projection, while the law enforcement and firefighter plans showed a surplus that made most of the combined projected surplus. He also identified a projected combined surplus in the multi‑billion‑dollar range in later years of his projection.

Pringle described cost‑of‑living adjustments (COLAs): some plans have capped, inflation‑based COLAs that allow up to 3% in a year, with excess inflation amounts "banked" for future years; other plans, including some PERS and TRS Plan 1 provisions, have no regular COLA but have received ad hoc increases in past legislatures. He said, "The plans 23 have a capped inflation based cost of living adjustment. So in a given year, they can receive up to 3% And to the extent that inflation is higher than that, that, that amount is banked." (quoted verbatim)

Pringle explained rules on post‑retirement employment for workers who continue in jobs covered by state retirement systems: retirees generally may work up to 867 hours per year for system employers without a benefit reduction. "These restrictions, however, are restrictions on pension payments, not whether you can work," he said, clarifying that retirees may exceed the limit but would have benefits suspended for the remainder of the calendar year if they do so while in covered employment.

Representative Levitt asked whether service years from a school district retirement system could be combined with PERS Plan 2 service for eligibility and benefit calculations. Pringle said portability rules generally allow years of service from different defined‑benefit systems to be combined for eligibility and benefit calculations, though the combined benefit cannot exceed what would be payable if all service had been rendered under a single system. "It's a great question. And most of the retirement systems for their defined benefit part of their their their benefits are combinable, through a a system that's called portability or the dual member benefits," he said.

On recent federal legislation, Pringle told the committee the Social Security Fairness Act, signed Jan. 5, removed the Windfall Elimination Provision and Government Pension Offset that previously reduced Social Security benefits for some workers who spent portions of their careers in Social Security‑exempt public jobs. Pringle said the elimination of those provisions can materially increase combined benefits for affected retirees and surviving spouses.

Committee members asked several clarifying technical questions and Pringle answered with program details and examples, including how supplemental benefits for higher education employees hired before 2011 remain in place for those workers and how Plan 3 differs as the defined‑contribution component.

There were no formal motions or votes recorded on the topic during the meeting. The session concluded after questions; members were not asked to take action during the presentation.

Ending: The committee received the presentation and asked technical questions; no formal decisions were taken during this briefing.