Sandy Springs retains AAA credit ratings; advisers say city can borrow but urge caution

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Financial adviser David Cheatwood told the council the city maintains AAA ratings from Moody's and S&P, has strong reserves and capacity to issue new debt; advisers estimated $60–$76 million of new borrowing could likely be absorbed without downgrading, while policy limits could technically allow much more.

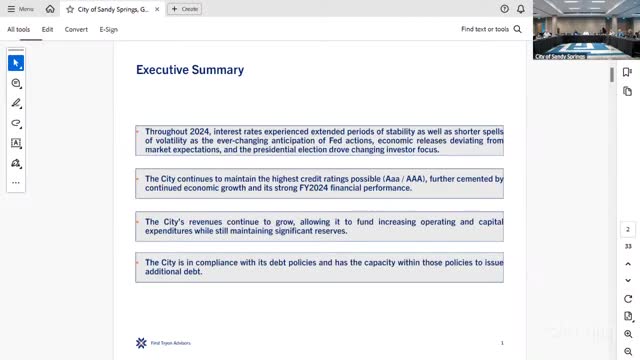

Sandy Springs officials were told at their annual council retreat that the city remains in strong financial health, holding AAA ratings from Moody's and Standard & Poor's and large reserve balances that give the city room to consider future borrowing.

David Cheatwood, the city's outside financial adviser, told the council the city's audited fiscal‑year 2024 results show robust revenues, steady annual debt service of about $12.6 million and fund balances that provide flexibility for capital spending. He said rating agencies cited a sizable tax base, high income levels and strong reserve and management practices when affirming the top ratings.

That rating and the city's financial position matter because they affect borrowing costs and how much capacity the council has to fund projects without increasing investor risk, Cheatwood said. He summarized three common ways to measure capacity: what current revenues can support, how much the scorecard could absorb without a downgrade, and the limits set by the city's own policies.

Using the city's 2024 results as a baseline, Cheatwood presented modelled scenarios. Relying on the roughly $5 million that flowed to fund balance in fiscal 2024 as a repeatable annual source, he said the city could support roughly $64 million of new 20‑year debt under the stated repayment assumptions. Using rating‑agency scorecards, he estimated the amount that could likely be added before the scorecard would move a notch down is about $76 million. By contrast, purely complying with the city's debt‑to‑full‑value policy would technically allow a much larger issuance—he cited a theoretical maximum of about $256 million—while another policy test (debt service as a share of revenues) produced a different upper bound (roughly $165 million under static revenue assumptions).

Cheatwood cautioned that the larger policy ceilings are theoretical and that affordability, revenue projections and potential below‑the‑line adjustments by rating agencies all affect outcomes. "If the goal is to preserve the AAA rating, that tends to put practical capacity in the $60 million to $75 million range," he said.

Council members asked what types of capital could be financed and about the mechanics of a bond referendum. Cheatwood advised that quality‑of‑life referendums such as parks and trails historically perform well if they include broad public engagement, geographically distributed projects and clear information about tax‑bill impacts rather than only headline dollar amounts.

City staff and advisers also reviewed specific balance‑sheet items that underpin the ratings. Cheatwood reported an unassigned general‑fund balance of about $35.7 million at fiscal‑year end, assigned fund balance of roughly $31.5 million, and a capital projects fund balance reported near $44 million; together those buckets give the city roughly $111 million of available resources by the measures he described. Outstanding principal was presented at about $207 million, and annual debt service was shown at roughly $12.6 million.

No formal decision was taken at the retreat. Council members pressed staff for follow‑up information on options, including public outreach and the projected property‑tax impact of any referendum, and staff said they would return with more detailed scenarios should the council direct them to pursue one.