Senate finance language proposes homestead exemption to replace statewide property tax credit

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

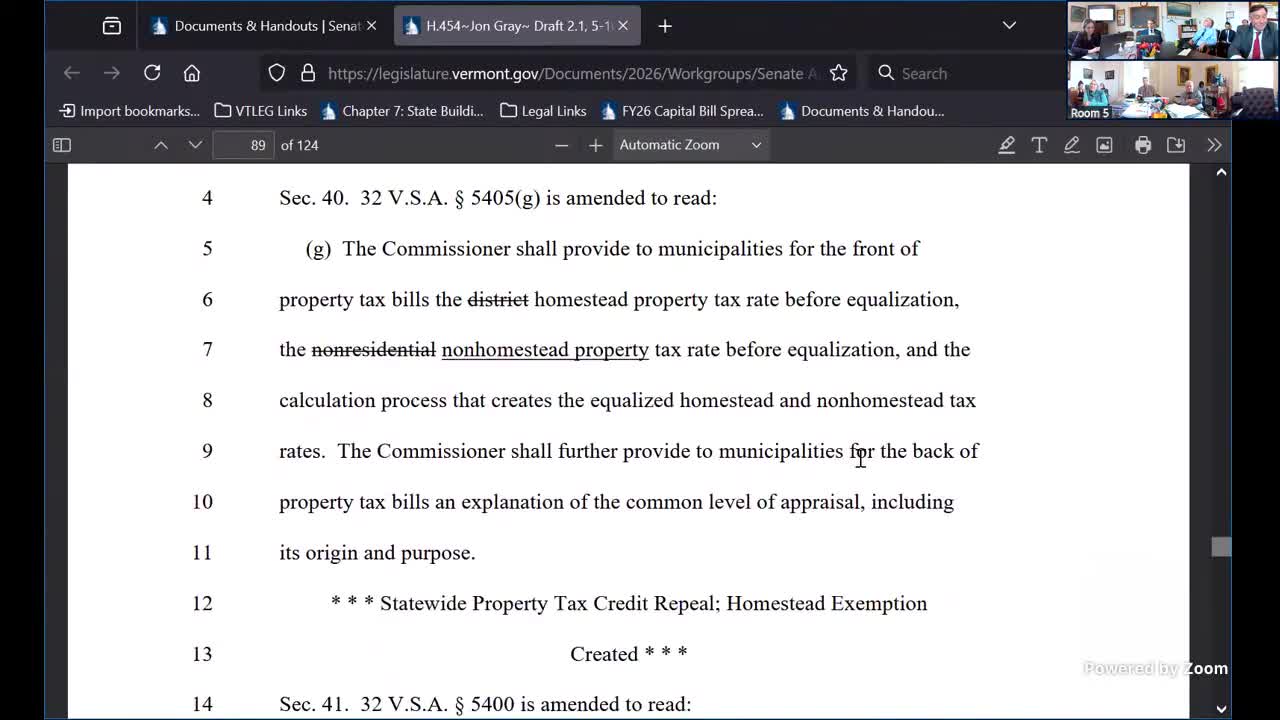

H.454 as amended by Senate Finance would repeal the statewide Property Tax Credit and replace it with a graduated homestead exemption tied to household income and a housesite cap (e.g., $425,000/$400,000 tiers); committee staff presented modeling of estimated bill impacts by income and house-site value.

H.454 includes language, new from Senate Finance, to repeal the statewide Property Tax Credit (PTC) and replace it with a homestead property tax exemption keyed to household income and a housesite value cap.

Under the Senate Finance configuration shown to the committee, an eligible claimant with household income at or below $100,000 would receive a percentage exemption applied to the first portion of housesite value — in many income bands the exemption would apply to the first $425,000 of housesite value for lower income bands and $400,000 for higher bands. The bill sets tiered income brackets with stepped exemption percentages (for example, very low-income households near $0–$2,000 would receive a 99% exemption on the applicable housesite cap; higher income bands receive progressively smaller percentages up to a 5% exemption at the top of the band approaching $100,000). The municipal-level property tax credit and municipal circuit breaker are retained.

Julie Richter, Joint Fiscal Office, presented modeling charts that compare the Senate Finance homestead-exemption design against current law income-sensitivity (the PTC). The committee was shown a chart that maps household-income buckets against assessed housesite value and displays estimated average dollar increases or decreases relative to FY2025 average net education property tax liability. Richter said the Senate Finance configuration was modeled to cost about $1.6 million less than current-law income sensitivity and was calibrated to direct greater average reductions toward lower-income households and lower housesite values.

Committee discussion focused on distributional impacts. Senators noted cliff effects around existing PTC thresholds (for example, the program structure under current law changes at $90,000 of income), and several members asked whether the housesite caps and percentage steps could increase tax liability for middle-income households in high-market-value areas. Staff emphasized the Senate Finance version was only one configuration; the Department of Taxes was tasked to produce alternative designs and a report by Jan. 15, 2026, on options that would minimize property-tax impacts.