Article not found

This article is no longer available. But don't worry—we've gathered other articles that discuss the same topic.

House hearing on House Bill 2454 proposes legislative audit officer to staff JLAC, separate performance audits from constitutional financial audits

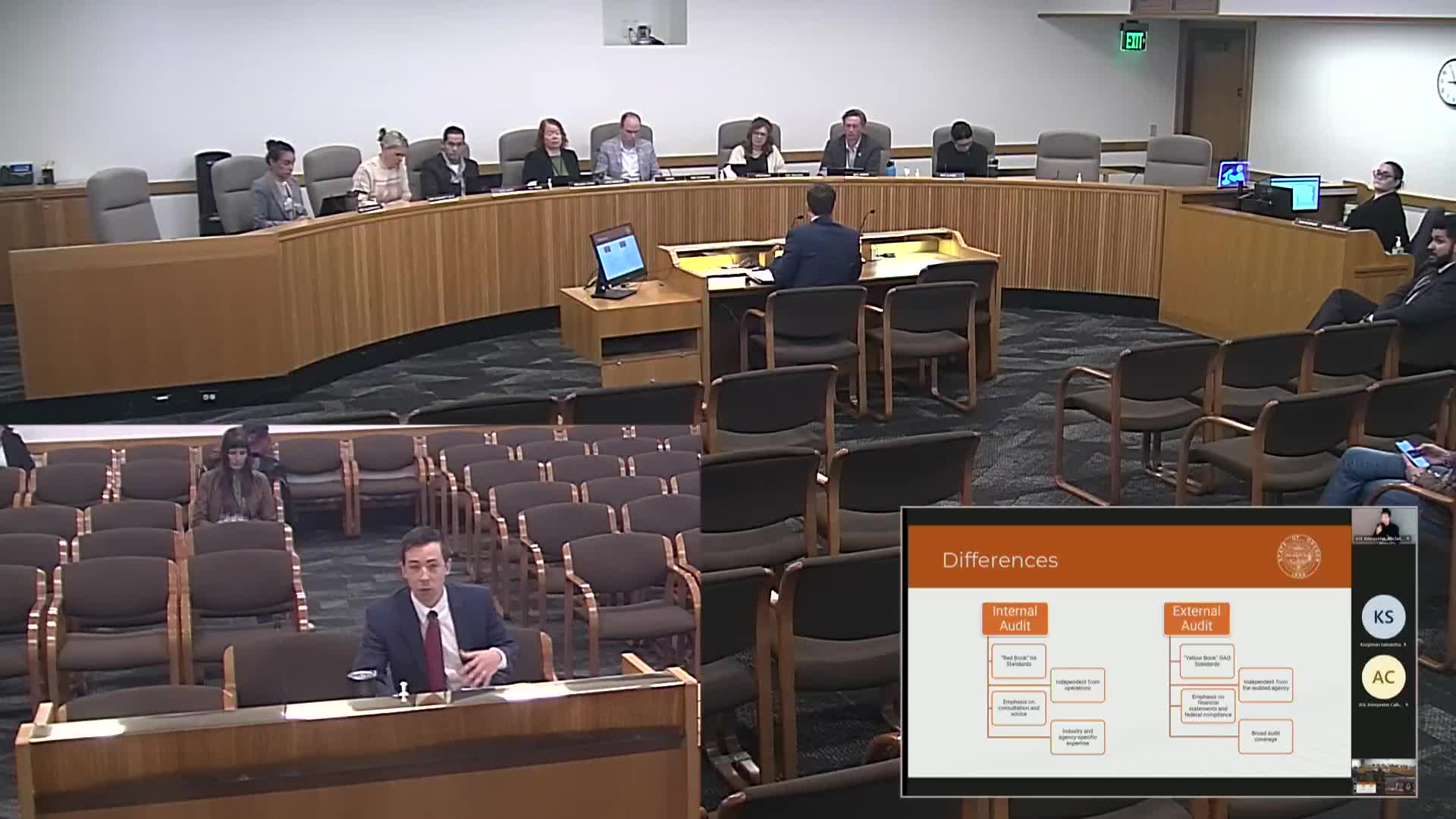

Department of Administrative Services outlines internal-audit standards, three-lines model and recent agency compliance gains

Secretary of State auditors outline FY26 plan, push for data-driven risk model and greater transparency